Global Oil Production Forecasts: What To Expect in a Shifting Energy Landscape

Global Oil Production Forecasts: What To Expect in a Shifting Energy Landscape

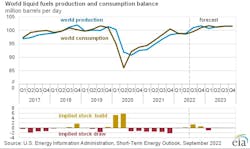

Forward to 2030, oil production trends are poised to reshape energy markets, with global output expected to stabilize—or subtly shift—amid structural changes across supply and demand. Global forecasts reflect a complex interplay of geopolitical dynamics, technological innovation, and climate pressures, making the next decade critical for energy planners, investors, and policymakers alike. Historically, oil output climaxed in the mid-2000s, but recent trends reveal a more nuanced evolution, marked by regional divergence, renewed investment in resilience, and cautious optimism about long-term stability.

authoritative sources paint a picture where conventional sources peak, unconventional gains compensate partially, and new frontiers remain underexplored. The International Energy Agency (IEA) projects global crude oil production to reach a plateau around 2025–2027, driven by anchored supply in OPEC+ and North America, offset by gradual declines in mature basins. BP’s 2024 Statistical Review notes a similar pattern: despite volatility, total global output is projected to remain within a narrow 85–90 million barrels per day (mb/d) range through the end of the decade.

ExxonMobil and S&P Global reinforce this downward-to-stable trajectory, citing limited new discoveries and aging infrastructure.

The Erie Shale and Bakken formations, once engines of rapid expansion, have seen production plateau or decline slightly, according to the U.S. Energy Information Administration (EIA). “We’ve reached the late maturity of these plays,” explains David C.

Black, senior analyst at Energy Intelligence. “Oil from these warm spots now requires significantly higher investment per barrel to maintain output.” Yet unconventional sources—auguring from tight oil, deepwater, and heavy oil—are filling the gap. In the United States, shale output remains resilient despite early concerns about the 2014–2016 price crash, supported by improved drilling efficiency and capital discipline.

Heavy oil projects in Canada, particularly in the Athabasca region, although capital-intensive and environmentally scrutinized, continue to supply consistent volumes, reinforcing Canada’s role as a stable long-term contributor. Deepwater and polar exploration, though uncertain, represent pockets of future potential. Brazil’s pre-salt basins and offshore Guyana in South America exemplify high-reward, high-cost frontiers with production climbing steadily—Guyana alone could supply over 1.2 mb/d by 2030, according to TotalEnergies.

In contrast, Arctic development remains politically and technically constrained, limiting near-term impact.

The kingdom’s "Swung Default" pricing mechanism and Moscow’s production strategy aim to balance market share with revenue targets. “Saudi Arabia views itself as the global benchmark,” notes Fatih Öztürk, head of Middle East energy insights at IHS Markit. “Its strategy isn’t just about economics—it’s about influence.” The United States continues as the world’s largest oil producer, combining shale dynamism with robust refining capacity.

Despite political fluctuations, technological pace and private investment keep output volatile but generally on upward trajectories except during severe price downturns. China, India, and the Middle East are emerging as dual engines of demand and supply. China maintains strict domestic production caps but remains a major refining hub and strategic buyer.

India’s domestic output modestly rises while imports anchor supply—making it a key player in market balance. Meanwhile, Iraq, Iran, and the Gulf Cooperation Council states navigate internal and external pressures to ramp production, constrained by infrastructure limits and sanctions legacies. Market Uncertainty and the Risk of Sudden Shocks Despite long-term forecasts, oil markets remain fragile.

Geopolitical tensions, from the Russia-Ukraine war to Red Sea shipping disruptions, repeatedly spike prices and disrupt supply chains. The 2022 invasion triggered crude volatility exceeding 40% over six months, underscoring fragility even in high-output regions. Natural disasters, cyberattacks on critical infrastructure, and regulatory shifts further complicate stability.

Meanwhile, the accelerating energy transition introduces a countervailing force: declining long-term demand growth. The IEA’s 2023 World Energy Outlook projects global oil demand peaking by the late 2030s, pressuring producers to balance near-term output with investment discipline to avoid future oversupply. ExxonMobil CFO Kayinstituting this view: “We are producing more efficiently, financially disciplined, and preparing for a world with less oil—but not one where supply gaps vanish overnight.

Resilience, not just volume, defines the next era.”

Consumers, investors, and nations must prepare for a dual reality: oil remains vital but less dominant, with production trends increasingly shaped by economics, geopolitics, and energy security rather than pure supply growth. As historical peaks recede into memory, suppliers face a choice—expand with caution or innovate toward integrated energy models. The path forward is not about excess or collapse, but adaptation: optimizing existing assets, embracing carbon-mitigation technologies, and navigating a market where volatility coexists with strategic inflection points.

In managing global oil production, the real challenge lies not in forecasting output, but in steering an unpredictable, interdependent energy future with foresight and responsibility.

Related Post

Finding Comfort: The Best Shoes For Plantar Fasciitis — Step Into Pain-Free Living

Unlocking Proton Saga’s Engine: Mastering the Game’s Core Mechanics from the Manual

Boenge Could Hit Your Living Room: Can “Can You Play It?” Fix Real NYC True Crime Cases on PC or PS5?

Unlock the Premium Kitchen Experience: Find A Williams Sonoma Store Near You